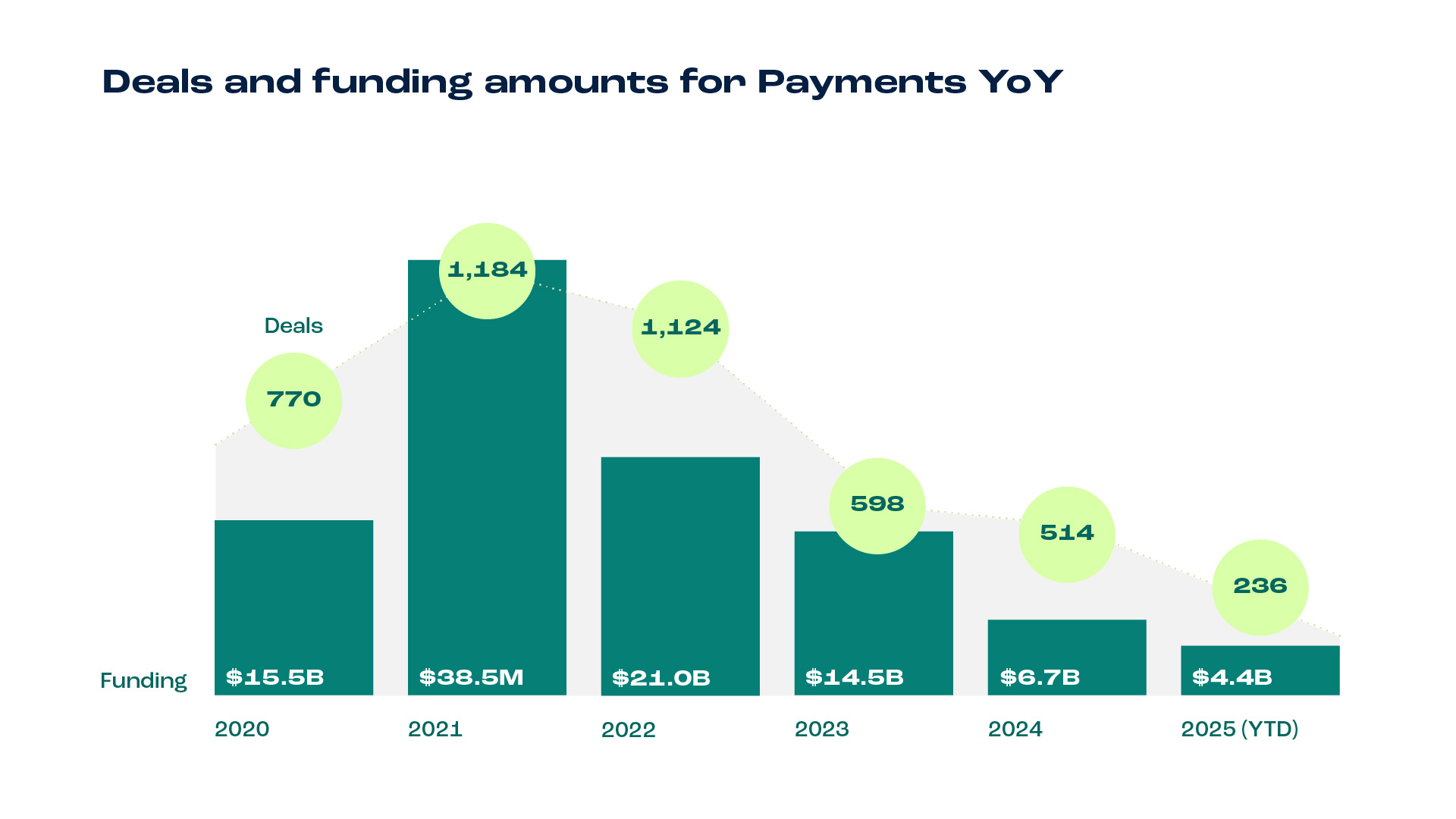

Funding in the payments space has shifted dramatically over the past five years. After record-setting funding years in 2021 ($38.5B), the venture market cooled in 2024 but is now showing signs of bouncing back. Investors are writing fewer checks, but for bigger amounts, betting on companies with traction and clear market positions.

2025 Payments Funding at a Glance

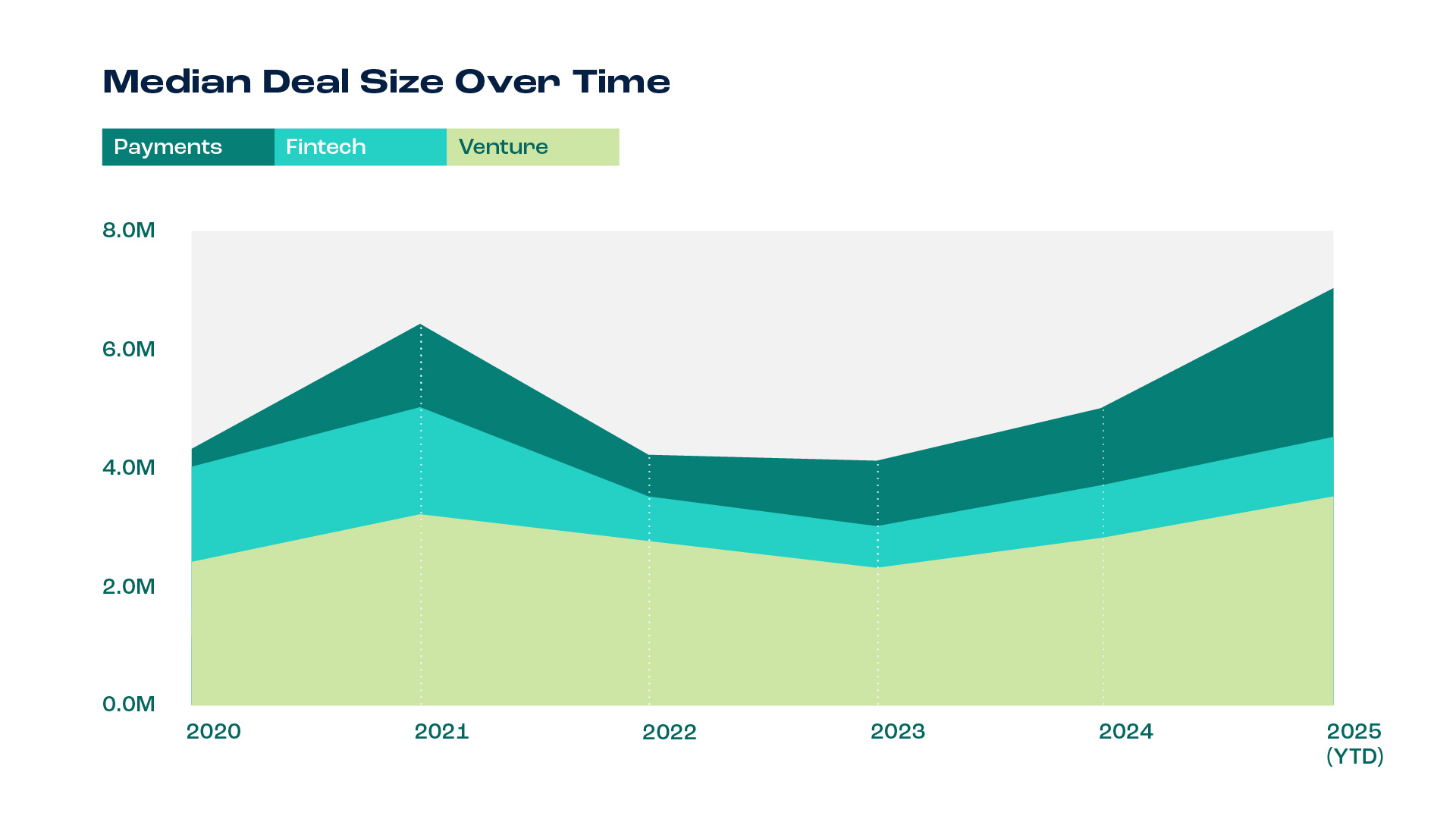

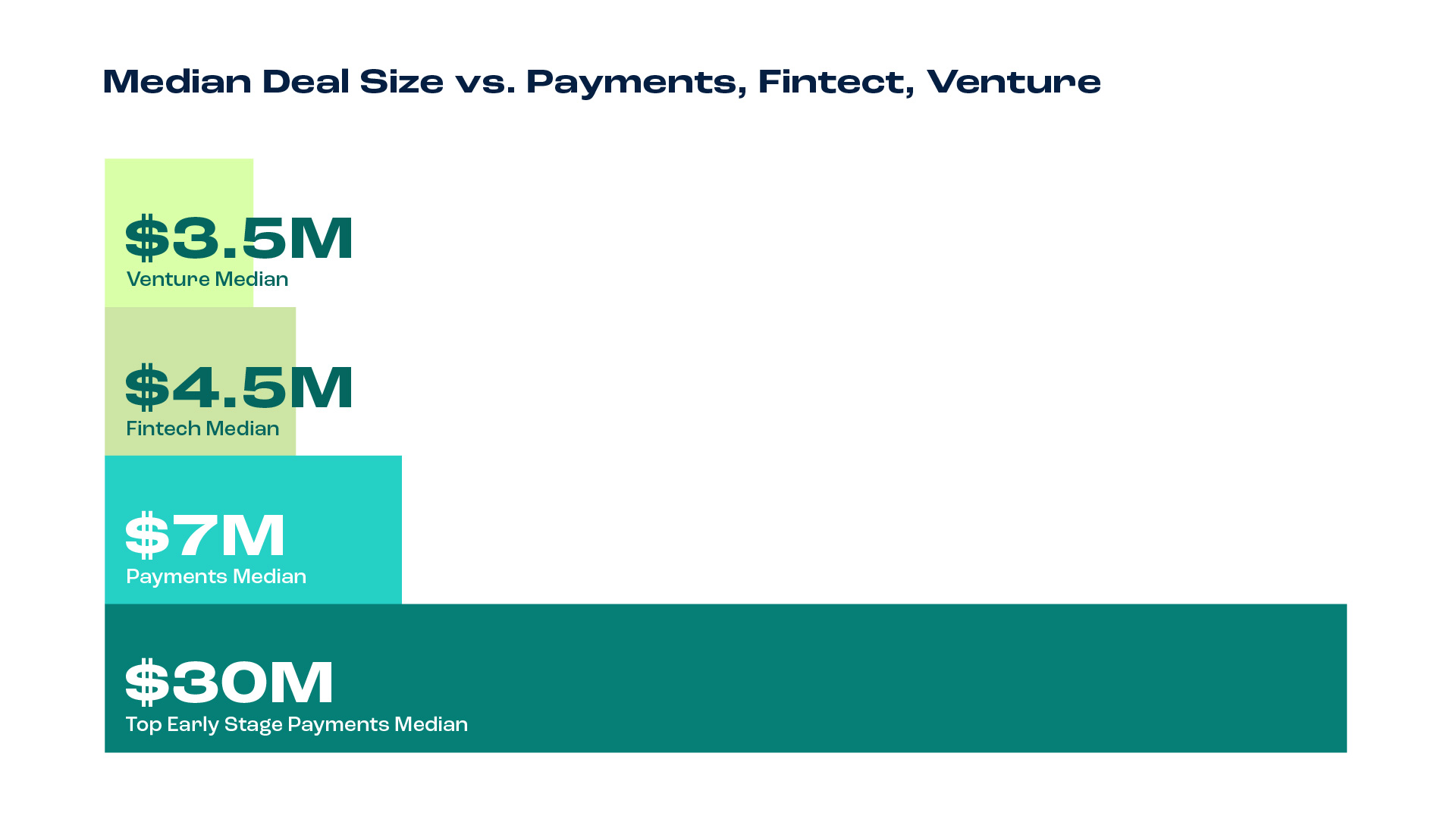

2025 is all about bigger checks for fewer startups. ****The median deal has surged to $7M—double the typical venture round and 1.55x the fintech median—marking the highest level since 2021.

[Chart] -> Show median deal size over time

Type of chart

- Multi-line Chart

- Area Chart

- Stacked Bar

- Multi-bar

Goal

- Want to be able to demonstrate the median payment amount of Payments vs. Fintech and Venture

See Chart Data Below

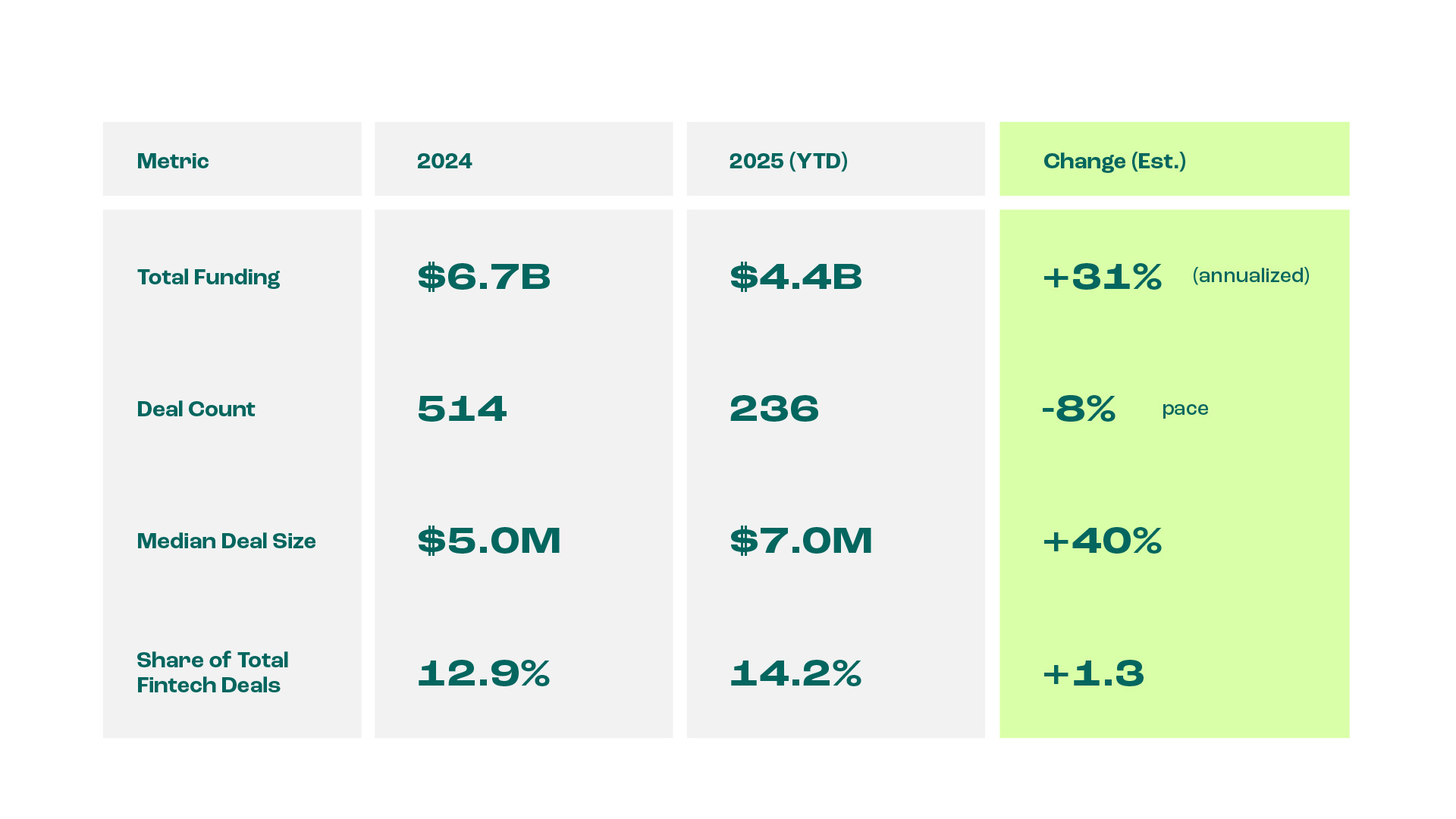

Year-to-date, payments startups have raised $4.4B across 236 deals, accounting for 14.2% of all fintech deals. Deal volume is pacing 8% lower than last year, but total dollars are tracking 31% higher, showing investors are betting selectively and with conviction.

Takeaway: Fewer checks, but larger ones. Investors are rewarding companies that can prove traction and product-market fit, not just growth potential.

Where the biggest checks are going

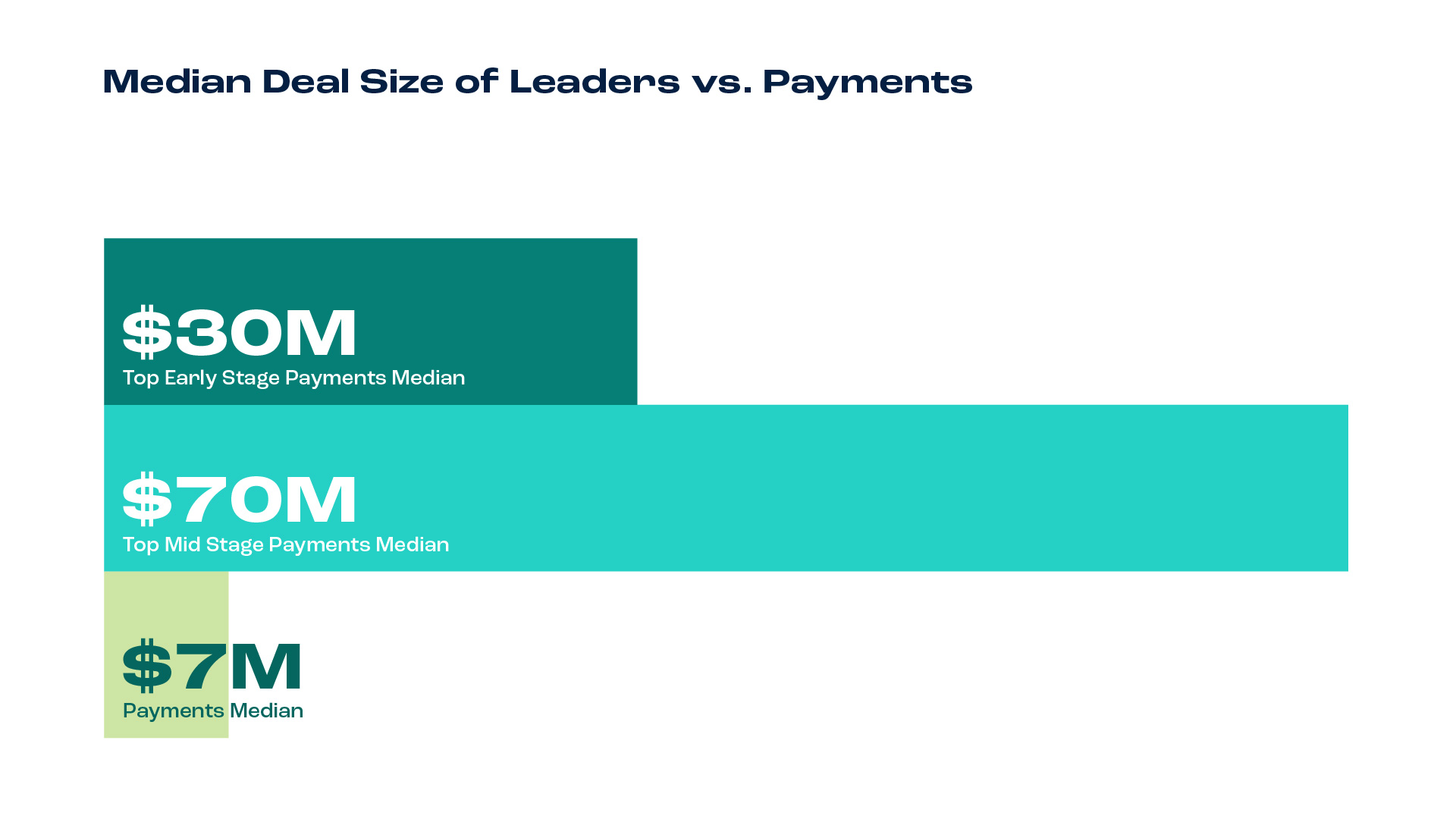

As we looked at the top early-stage and mid-stage* funding rounds in 2025, a clear pattern emerged: specialization wins. Investors are backing payments startups with vertical-specific or problem-specific focus, creating defensible market positions.

The median deal size for early-stage payments startups YTD is $30M, that’s over 4x the rest of the market ($7M). While mid-stage* rounds hit a median of $75M, over 10x higher than the median deal size.

Early-Stage Leaders (Pre-seed, Seed, Series A)

Median funding: $30M → 4.29x rest of payments

Mid-Stage Leaders (Series B only)

Median funding: $75M → 10.71x rest of payments

How 2025 Compares to Previous Years

The funding environment in payments reflects the broader post-boom fintech landscape. Even as deal volume remains below the 2021 peak, investors have recalibrated. Here are some trends we’re seeing

Median deal size is surging

At $7M, the median payments deal in 2025 is 2x the venture median and significantly higher than the fintech median ($4.5M). This marks the highest median deal size since 2019, a clear sign that investors are concentrating capital into startups that have proven traction and defensibility. Payments is increasingly a “big check” category, rewarding teams that demonstrate market readiness.

Key Insights

- Median payments deals are 2x the venture median and 1.55x the fintech median.

- Highest median deal size since 2019 signals concentrated investor confidence.

- Larger checks favor startups with traction and market defensibility.

Payments deal volume is pacing 8% lower year-over-year, yet total funding is tracking 31% higher. This divergence highlights a market that is highly selective but confident, willing to back fewer companies with meaningful checks. The capital concentration signals that investors are moving past the scattershot approach of 2021 and into a quality-over-quantity mindset.

Key Insights

- Deal count down 8% YoY, but funding up 31% shows selective optimism.

- Capital is consolidating into fewer, higher-value bets.

- Market signals strong support for category leaders over broad exposure.

Breakdown by funding stage

Series A and B rounds account for 63% of all 2025 payments deals, continuing a multi-year trend where early- and mid-stage companies attract the majority of dollars. Late-stage rounds remain scarce without a clear path to profitability or market leadership. The current breakdown of 2025 deals reflects this bias: 149 early-stage, 38 mid-stage, 28 late-stage, and 21 other.

Key Insights

- 63% of deals are Series A or B, confirming early/mid-stage dominance.

- Late-stage rounds are rare without clear profitability or leadership signals.

- Investor focus is on scalable companies with room for growth.

Specialization is a winning formula

The largest checks in 2025 have flowed to deeply specialized payment solutions, such as embedded finance, cross-border networks, and vertical-specific payment platforms. Broad, undifferentiated processors are being left behind, as investors increasingly favor startups that solve high-value, narrowly defined problems. This focus on specialization creates both defensibility and a faster path to meaningful market share.

Key Insights

- Specialized solutions are attracting nearly all major checks.

- Cross-border, embedded finance, and vertical-specific platforms lead the pack.

- Generalist payment processors are largely ignored by investors.

What All This Data Tells Us

It’s clear that funding a payments startup is no longer about chasing every idea—it’s about backing the best ones. After years of volatility, investors have shifted to a quality-over-quantity mindset, concentrating capital on startups that solve high-value, specialized problems.

For payments founders, this is both a challenge and an opportunity—fewer bets are being made, but the right bets are bigger than ever.

How We Collected and Analyzed the Data

To build this report, we started with raw data from:

- Crunchbase State of Fintech Reports (2021–2024, including Q1 and Q2 2025)

- Crunchbase State of Venture Reports (2021–2025, including Q1 and Q2 2025)

From there, we isolated the data most relevant to fintech and payments, including total dollars raised, number of deals, and stage distribution. We also pulled historical data going back to 2015, giving us a longer view of how funding in fintech and payments has evolved over the past decade. This perspective helps illustrate the rise, peak, and correction of the current venture market.

For the top companies of 2025 dataset, we focused on early-stage and mid-stage startups—pre-seed, seed, Series A, and Series B based in the US.

Q2 2025

Fintech Funding Report - Payments

Stay Connected

Q2 2025